Overview

One of the foundational economic principles taught in any Econ 101 course is that of specialization – that individuals and societies are more productive when they focus on producing goods / services they have a distinct advantage in producing and trade for those goods / services where others have a relative advantage over them.

A restaurant chain’s distinct advantage should (hopefully) be in the way it serves food to its customers (e.g., menu design, recipes, order execution, etc.). For many restaurants, this requires a physical footprint across many locations to serve local customer groups. Historically, restaurant entrepreneurs hoping to roll out a successful concept across the nation may have purchased real estate to operate restaurants out of – taking on not only the financial burden of real estate ownership (e.g., mortgage payments, interest, insurance, etc.) but also operational upkeep (maintenance and repairs, landscaping, etc.). For some businesses with significant real estate portfolios where the ownership and management of the properties is truly non-core to their business, there may be an opportunity for operational improvement and financial engineering through a transaction called a Sale-Leaseback.

A Sale Leaseback transaction is actioned by a business that owns a portfolio of real estate assets that it is the primary user / beneficiary of in its core business. Good examples are restaurant chains, retailers, grocery stores, or medical clinics. The business then finds a buyer or buyers of the real estate portfolio and negotiates a long-term lease to continue using the space as a tenant / lessee instead of an owner. The transaction involves several benefits and costs that need to be tallied up to determine whether or not the transaction is accretive or dilutive to an investment:

Costs | Benefits |

|---|---|

1. Addition of Lease Expense / Rent 2. Ceding some operational control to a third party lessor | 1. Large capital inflow from sale of real estate which can be reinvested into the business, used to pay down debt, or taken as a dividend 2. Forego ongoing mortgage payments / interest associated with owned property 3. Less operational distraction on managing the property if property manager handles day to day responsibilities |

Why do a Sale-Leaseback?

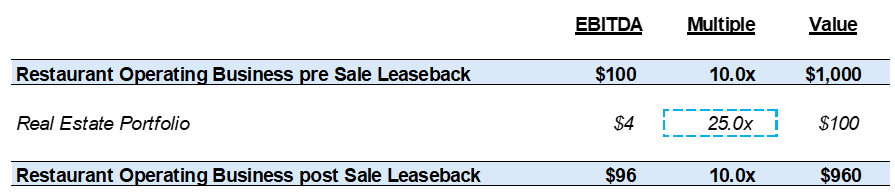

Cost of Capital Arbitrage. This is the primary reason. Real estate often trades at higher multiples / lower yields than the operating businesses that occupy their premises given the stable, predictable nature of real estate assets (vs. retail businesses susceptible to changing consumer whims). An extreme example – let’s say the restaurant business we described above has the following simplified valuation components:

Let’s say it also owns real estate worth $100 million based on a 4% Capitalization or “Cap.” Rate. For illustrative purposes, say this means a buyer would pay the restaurant chain $100 million for $4 million per year in lease payments in perpetuity (n.b., Cap. Rates are actually based on net income, not gross lease rate, but let’s oversimplify for the illustrative math here). What would that look like relative to the math we presented for the operating business?

Wow. 25x? Where did that come from? A multiple is always the inverse of a yield, and a Cap. Rate is just an undercover yield (Net Operating Income / Asset Value), and 1 / 4% = 25x. This layout much more clearly shows how much greater valued a dollar of real estate earnings is relative to restaurant earnings in this hypothetical scenario. Ok, so let’s put it together – what happens?

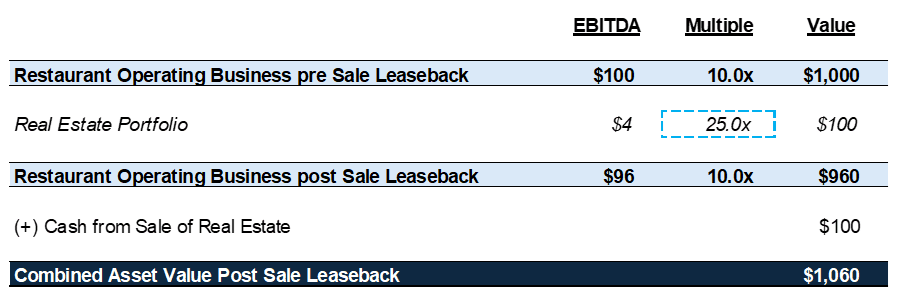

Well hold on. $960 is less than $1,000 – what happened to my accretive transaction? While it’s true that the operating business is now worth less given the lower EBITDA profile with the same multiple applied, the truth is we now own two assets – a $960 million operating business (burdened by new lease expense) and $100 million of cash burning a hole in our pocket:

Just like that, we created $60 million of value by drafting up a few contracts and reallocating assets to their optimal, specialized owners. Isn’t investing fun?

Increased focus on core operations. Particularly if the new owner also manages the real estate assets, the company can shift its focus entirely to its core operations instead of real estate related concerns.

Potential drawbacks.

Lesser control of an operationally important asset. For anyone who’s rented real estate, you know that the wrong landlord can make life miserable. Choosing a high quality real estate owner and manager and negotiating a long-term lease with cost visibility is key to ensuring operations run smoothly post sale leaseback and the deal continues to be attractive financially.

A Note on "PropCo" Spin-offs

This concept applies not only to private equity deals where sponsors will action these deals to benefit from the cost of capital arbitrage during their hold period – but also to large, publicly traded retailers through a Property Trust or Real Estate Investment Trust (“REIT”) spin-off where the retailer would split its operating company (OpCo) from its real estate, putting the latter into an independent property company (PropCo), setting up the lease agreement between the OpCo (lessee) and PropCo (lessor), and listing the PropCo as a separate publicly traded company. Below are two examples from a U.S. restaurant chain and a Canadian grocer – the latter of which I had the pleasure of working on as an Investment Banker in a previous life:

Modeling Sale Leasebacks

The following paragraphs and exhibits provide a framework for how to model a Sale-Leaseback transaction from first principles, as well as a discussion on the rationale for each step and how this transaction links into the Six Core Schedules of the base LBO. Follow these steps to build Sale-Leasebacks into a model outside of Mosaic (i.e., in Excel). For an Excel copy of the below analysis, reach out to your Mosaic Account Executive or sales@mosaic.pe.

A digital Sale Leaseback model is available in Mosaic under “Special Situations” to save you from needing to repeat these steps and reduce manual error. See our help article below on how to add Sale Leasebacks to your Mosaic model:

Mosaic Special Situations | Sale Leaseback

As shown in our simple example above, the Sale Leaseback transaction has two main elements that need to be reflected in a deal model:

Sale Leaseback Proceeds. This is the after-tax amount of cash received for the sale of properties involved in the transaction.

Starting Annual Rent. This is the amount the business will need to pay annually for continued use of the properties after the sale is completed. We call this “starting” because often some sort of inflationary rent escalator will be applied each year, growing the annual cost to the business.

As well as two other potential parameters to consider:

Annual Rent Increase. A percentage amount of increase on the beginning rent, applied each year (often contractually under a long-term lease with the lessor).

Sale Leaseback Year. Most investors buying a business with a large non-core real estate portfolio will identify the Sale Leaseback opportunity and plan to action it immediately (i.e., in Year 1 of their ownership). If that is not the case, you may want a dynamic assumption to pick which year within the investment hold period you want to action the Sale Leaseback (e.g., if you have another value creation plan priority before distracting the team with the Sale Leaseback or if you want to wait for a more favorable Cap. Rate environment, etc.).

Desired Goal:

So long as your assumed multiple of Sale Leaseback Proceeds / Annual Rent is greater than your assumed exit multiple for the business, the Sale Leaseback transaction should increase both IRR and MOIC as the benefit of the proceeds received will outweigh the reduction in exit value from a reduced annual EBITDA.

The Sale Leaseback is a Model Extension in Mosaic and we will discuss its impact on the Six Core Schedules of the LBO covered in our foundational article on the Anatomy of the Deal Model.

Sale Leasebacks impact the following schedules:

Step 0 – Sale Leaseback Assumptions

As with any deal modeling exercise, it’s helpful to start by setting up an assumptions bank that clearly separates your chosen inputs from the mechanics of the model itself. The key assumptions you need to make space for before building anything are:

Sale Leaseback Proceeds

Starting Annual Rent (mm)

Annual Rent Increase (%)

SLB Date

Here’s an example of what the Sale Leaseback Assumptions bank looks like in Mosaic’s Excel download:

Step 1 – Layer Sale Leaseback Rent Expense into EBITDA

Impacts: OPERATING MODEL

The first and most impactful adjustment we must make to the deal model for the Sale Leaseback is layering in the annual rent expense into our operating model.

In Mosaic, we create a new tab called a “Consolidated” tab which copies over the core lines of the operating model (i.e., Revenue, EBITDA, Capex, and NWC) and expands them for inorganic model extensions like M&A, cost savings plans, sale leasebacks, etc.

If you’re building a simple model with one operating case and cost savings, you can layer this directly into your operating model. Mosaic supports multiple operating cases (e.g., upside, downside, base, management case, etc.) which necessitates an additional consolidated tab to layer on inorganic model extensions.

Let’s add a line for the Sale Leaseback rent impact to EBITDA. This line will need to model out the starting rent plus the annual rent increase factor that we’ve assumed as well.

Below is a GIF illustrating the formula we apply for layering in Sale Leaseback rent:

Step 2 – Sale Leaseback Proceeds

Impacts: FREE CASH FLOW

The one time benefit we receive from selling the real estate must also be reflected in our deal model – however, this is a non-recurring benefit and thus does not impact EBITDA or the operating model. As such, we reflect the Sale Leaseback proceeds in the cash flow statement to ensure that we are appropriately benefiting our cash flows with the one-time inflow so that it is reflected as a source to pay down debt, etc.

Again, below we show a GIF to reflect how we layer the Sale Leaseback proceeds into the model, including the timing assumption for the Sale Leaseback transaction.